Arm Holdings’ growth story could be just getting started as new products and services emerge from the chip revolution.

A couple of years ago, semiconductor specialist Nvidia attempted to acquire a little-known company called Arm Holdings (ARM 6.84%).

Unfortunately for Nvidia, the company abandoned the deal as long-winded court cases revolving around antitrust concerns seemed to have no end in sight. Following the failed acquisition, Arm pursued an initial public offering (IPO) — hitting the Nasdaq last September.

Since going public, Arm stock has surged 138% on the backdrop of the artificial intelligence (AI) movement. But even after such a meteoric rise, I see much better days ahead for Arm. In fact, I think Arm stock will handily outperform Nvidia over the next decade.

Below, I’ll detail why I’m so bullish on Arm and explain how rising competition in the chip realm could ignite Nvidia’s first uphill battle in quite some time.

Why Arm stock might outperform Nvidia

The semiconductor industry has many different components. Not all chip companies make graphics processing units (GPUs) like Nvidia or Advanced Micro Devices. There are far more applications for chips, and Arm dominates a pretty singular pocket of the market.

At its core, Arm designs chip architecture for mobile devices, consumer electronics, networking equipment inside data centers, and other Internet of Things (IoT) devices. The company makes money from licensing out its intellectual property (IP), and earns a royalty based on its various architectures.

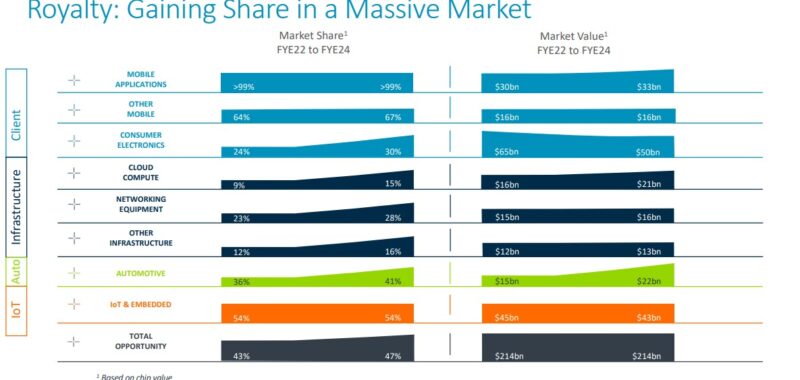

Image source: Arm Holdings Investor Relations.

As illustrated in the graphic above, Arm’s architecture is deeply embedded across various applications. This provides the company with an enviable level of flexibility regarding new chips hitting the market in the future. In other words, companies running on Arm’s architecture are less inclined to develop a new hardware and software system that is incongruent with Arm’s architecture.

Furthermore, the slide above shows that Arm’s market share has increased across the board over the last two years. With that in mind, I think the company is well positioned to continue benefiting from new chip-based devices, since Arm’s IP is already leveraged across so many devices around the world.

For this reason, I see Arm as less vulnerable to competitive forces in the chip space compared to peers such as Nvidia.

Why Nvidia’s best days may be in the rearview mirror

Like Arm, Nvidia has a massive presence in its core end market. The company’s A100 and H100 chipsets have helped Nvidia acquire an estimated 88% of the GPU market.

However, I see some obvious risks that could expose Nvidia over the next several years, and I would not be surprised to see the company begin to lose market share.

First, companies including Microsoft, Alphabet, Tesla, Amazon, and Meta Platforms are all investing in their own custom chip designs. Moreover, these companies have been labeled by Wall Street analysts as Nvidia’s largest customers — accounting for nearly half of the company’s revenue.

While you could argue that more competition is a good thing for Nvidia, I don’t see it that way in this case. These companies will probably remain customers of Nvidia for the next several years, but the introduction of their own hardware could wind up being a bargaining chip in the long run.

What I mean by that is that more GPUs on the market will likely weaken Nvidia’s pricing power. In turn, I think Nvidia’s revenue and profit growth could have a dramatic slowdown — a dynamic that growth investors won’t want to see.

But rising competition isn’t the only risk facing Nvidia. Given the company’s near-monopoly position, there is a possibility that the Department of Justice (DOJ) could investigate Nvidia’s business practices and force the company to loosen up its ecosystem.

With so many unknowns revolving around Nvidia’s future, I’m skeptical that the stock is a no-brainer at this juncture.

Is Arm stock a buy right now?

There have been many periods of expansion and contraction in Arm’s trading activity. But with a forward price-to-earnings (P/E) multiple of 96, it’s hard to say the stock is cheap.

The forward P/E of the S&P 500 is about 23, less than one-quarter that of Arm.

ARM PE Ratio (Forward) data by YCharts.

Here’s how I think about it: The market is clearly placing a premium on Arm stock for a reason. I think there are two core themes to unpack.

At a macro level, AI appears to be here for the long run, and technology‘s biggest companies are committed to spending billions on future artificial intelligence initiatives. While spending will change from year to year, the secular tailwinds presented by AI should bode well for Arm.

At a company-specific level, Arm’s unique position in the chip space and its lucrative business model suggest that the company’s growth will remain robust over time.

For these reasons, I see Arm as the superior investment over Nvidia in the next decade. While the stock isn’t a bargain, I think it still looks like a compelling opportunity for long-term investors.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.